Why Retirement Planning Matters

Retirement is often seen as the ultimate goal after decades of hard work.

But achieving a comfortable and stress-free retirement doesn’t happen by chance – it requires careful planning and execution.

Whether you dream of traveling the world, spending time with family, or simply enjoying a slower pace of life, taking the right steps now can make all the difference later.

Let’s dive into the 10 essential steps to plan the perfect retirement.

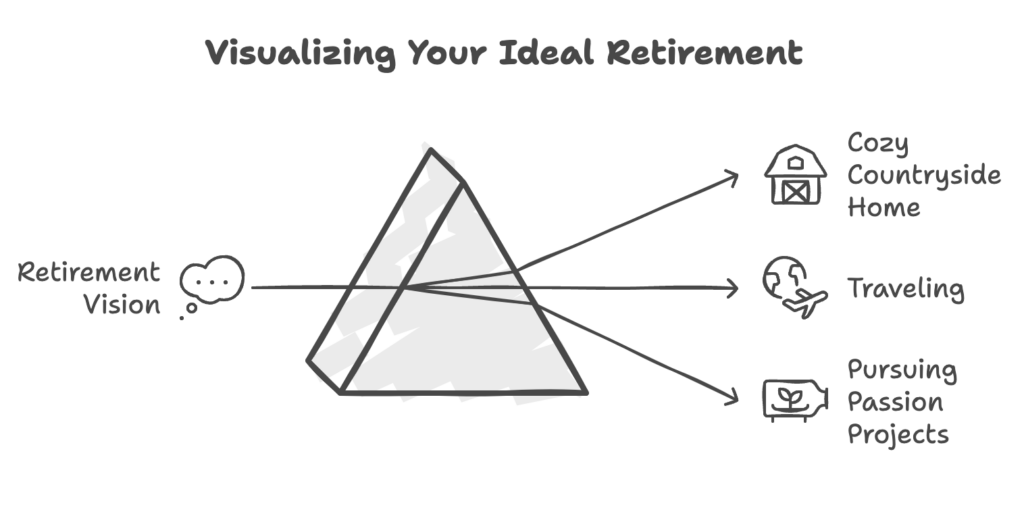

Step 1: Define Your Retirement Goals

What Does Retirement Look Like to You?

Retirement is a deeply personal experience. Ask yourself: Do you see yourself living in a cozy countryside home, traveling, or pursuing a passion project? Defining your vision provides clarity and direction.

Balancing Dreams and Reality

While it’s great to dream big, remember to balance your aspirations with practical considerations like finances and health. Prioritize what truly matters.

Step 2: Assess Your Current Financial Situation

Understanding Your Net Worth

Start by calculating your assets and liabilities. Knowing where you stand financially will help identify gaps in your retirement planning.

Analyzing Income and Expenses

Step 3: Determine Your Retirement Needs

Calculating Retirement Expenses

Estimate your future expenses based on your desired lifestyle. Don’t forget to include housing, food, transportation, and entertainment.

Factoring in Inflation and Healthcare Costs

Inflation can erode the value of savings over time, and healthcare costs tend to rise with age. Plan accordingly to ensure these don’t derail your retirement.

Step 4: Build a Retirement Savings Plan

Utilizing Employer-Sponsored Plans

If your employer offers a retirement savings plan, take full advantage of it, especially if there’s an employer matching component.

These contributions can significantly boost your retirement fund over time and offer a reliable foundation for your savings strategy.

Maximizing Planes Personales de Retiro (PPRs)

Planes Personales de Retiro (PPRs) are an excellent option for growing your retirement nest egg. These plans function similarly to IRAs in other countries, offering tax advantages and long-term growth potential.

Explore the options available and ensure your contributions align with your financial goals.

Step 5: Diversify Your Investments

Importance of Asset Allocation

Diversifying your portfolio across stocks, bonds, and other assets reduces risk and enhances growth potential.

Risk Tolerance and Time Horizon

Your investment strategy should reflect your risk tolerance and how many years you have until retirement.

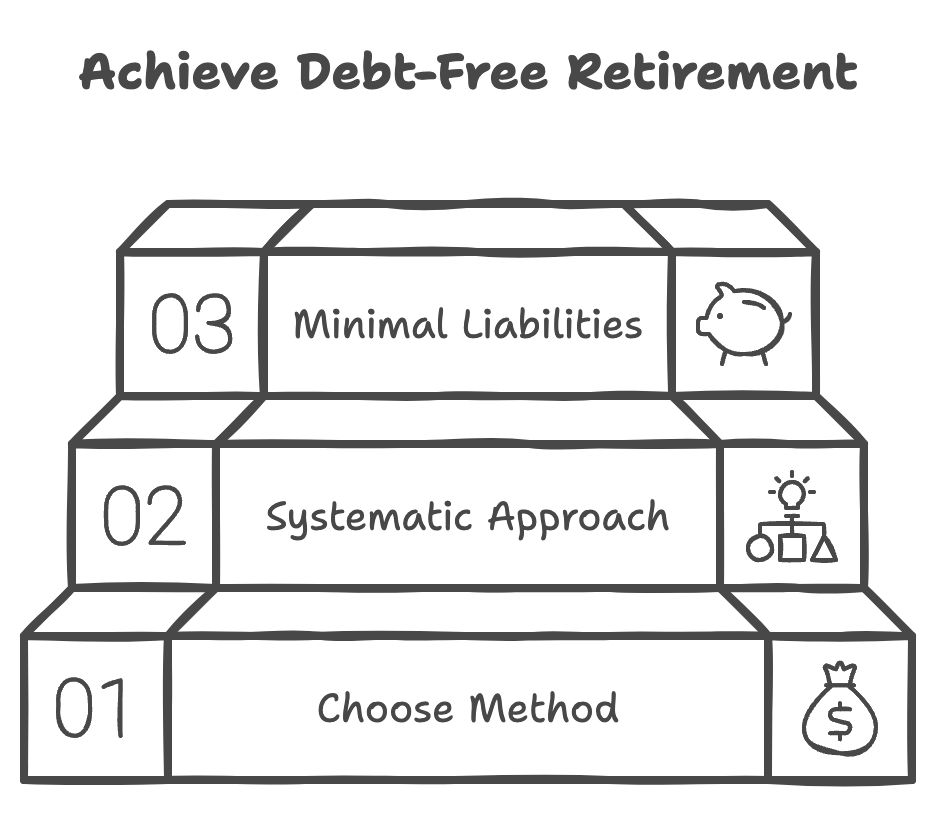

Step 6: Eliminate Debt

Prioritizing High-Interest Debt

Focus on paying off credit card debt and other high-interest obligations first. They can significantly hamper your financial freedom.

Strategies for a Debt-Free Retirement

Consider consolidation or snowball methods to systematically tackle debt. Aim to enter retirement with minimal liabilities.

Step 7: Plan for Healthcare

Savings for Healthcare Insurance

Healthcare costs vary significantly by location and personal circumstances. If you’re in Mexico, budgeting for private health insurance is key.

Research insurance providers to find a plan that meets your needs and ensure your savings plan accounts for these incremental changes.

Step 8: Focus on Savings and Lifestyle Preparation

Lump Sum Investments and Monthly Savings Plans

Passive income strategies like dividend-paying stocks can play a role in retirement planning when incorporated into mutual funds. These dividends are often reinvested into your savings plan, contributing to long-term growth.

Prioritize financial strategies such as lump sum investments for short-term growth (3-5 years) and monthly savings plans for long-term stability (15-25 years), ensuring a disciplined approach to building your retirement fund.

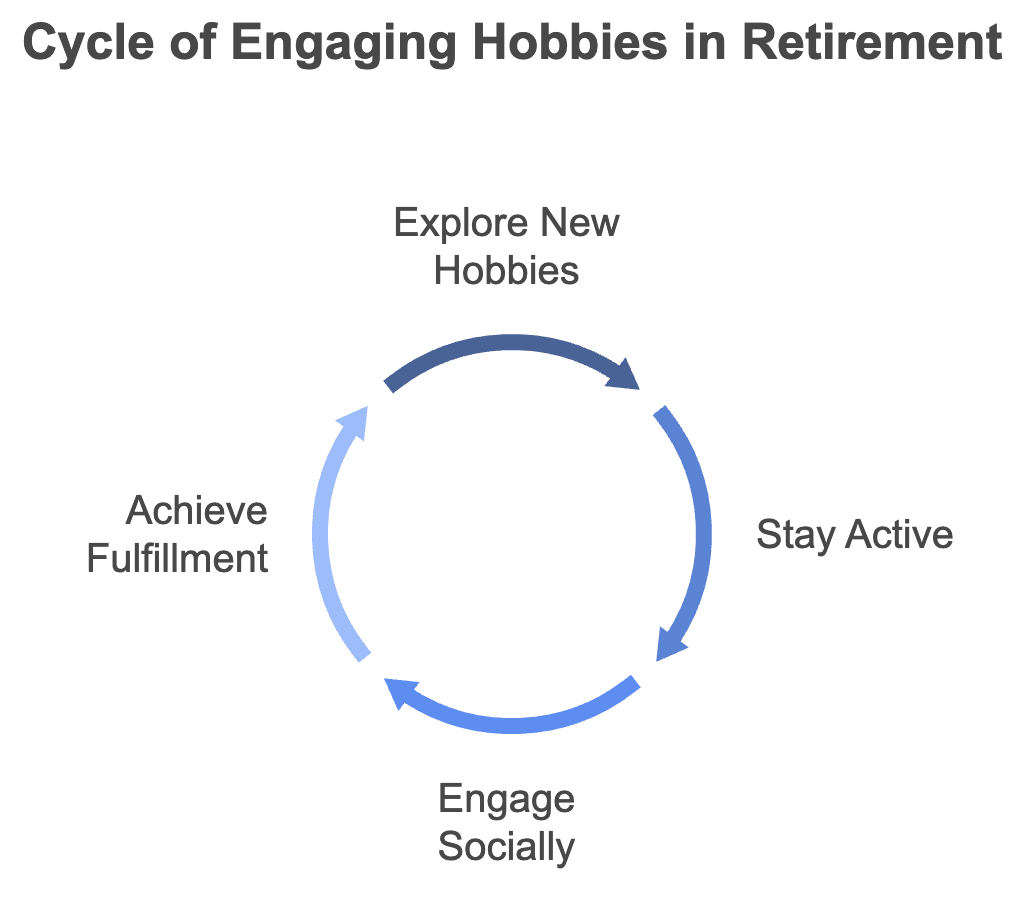

Step 9: Prepare for Lifestyle Adjustments

Exploring New Hobbies and Interests

Retirement is the perfect time to embrace hobbies and activities you’ve always wanted to pursue. However, it’s essential to factor these into your retirement budget.

For example, maintaining a health club membership for your family, which may cost around $350 a month, can add significant value to your quality of life during retirement.

Identifying these costs early allows for better financial preparation and ensures you can enjoy the lifestyle you envision.

Step 10: Create a Legacy Plan

Building a Financial Legacy

Creating a legacy is more than just a financial strategy – it’s about leaving behind stability, independence, and opportunities for your loved ones.

Start by understanding the potential consequences of not planning effectively: dependence on children or family, financial strain, and missed opportunities for a comfortable retirement.

By taking proactive steps now, such as lump sum investments and monthly savings plans, you can ensure a great life in retirement.

These strategies allow you to remain financially independent and build a nest egg that can be passed on to your loved ones.

Providing for Future Generations

A well-crafted financial legacy ensures your loved ones benefit even after you’re gone. This might include an inflation-linked income they can rely on for years or a lump sum they can use as they choose.

By planning wisely, you not only secure your financial freedom but also leave behind a gift of stability and choice, ensuring that you’re remembered for empowering your family rather than being a financial burden.

Planning the perfect retirement may seem overwhelming, but breaking it down into these 10 steps makes the process manageable.

Start now, and remember that every small step brings you closer to your dream retirement. The earlier you begin, the more time you’ll have to enjoy the fruits of your labor.

FAQs

- What age should I start planning for retirement?

Ideally, start planning in your 20s or 30s, but it’s never too late to begin. - How much money do I need to retire comfortably?

This depends on your lifestyle, but financial experts recommend aiming for 70-80% of your pre-retirement income. - What is the 7% Rule in Retirement Planning?

To meet your target income, we can calculate how much you need to save based on withdrawing a set amount each year and reinvesting a portion to cover inflation. - Can I plan for retirement if I’m already in my 50s?

Absolutely! While starting earlier is better, you can still make significant progress with focused saving and investing. - How can I manage retirement savings during economic downturns?

By saving monthly, you can benefit from market downturns by purchasing more units at lower prices, maximizing returns over the full lifespan of your plan rather than focusing on short-term performance.